Dec 23 – Welcome to the home for real-time coverage of markets brought to you by Reuters reporters. You can share your thoughts with us at markets.research@thomsonreuters.com

DOES CRYPTO GET A “SANTA RALLY” OR LUMP OF COAL IN DECEMBER? (1356 EST/1856 GMT)

Markets have been juggling worries over the Omicron variant of coronavirus over the past weeks, and cryptocurrencies have not been immune.

Register now for FREE unlimited access to Reuters.com

As per cryptocurrency research firm CryptoCompare, total inflows into digital asset products turned negative in December’s third week. That marks the first time since mid-August.

Average daily volumes also dipped from the start of the month through December 20, slipping 1.4% to $659 million. In January, they stood at $1.51 billion.

However, digital products along with other risky assets have caught some Christmas cheer from the so-called “Santa Claus rally” this week. Bitcoin is up about 8% so far this week, on track for its best week in two months.

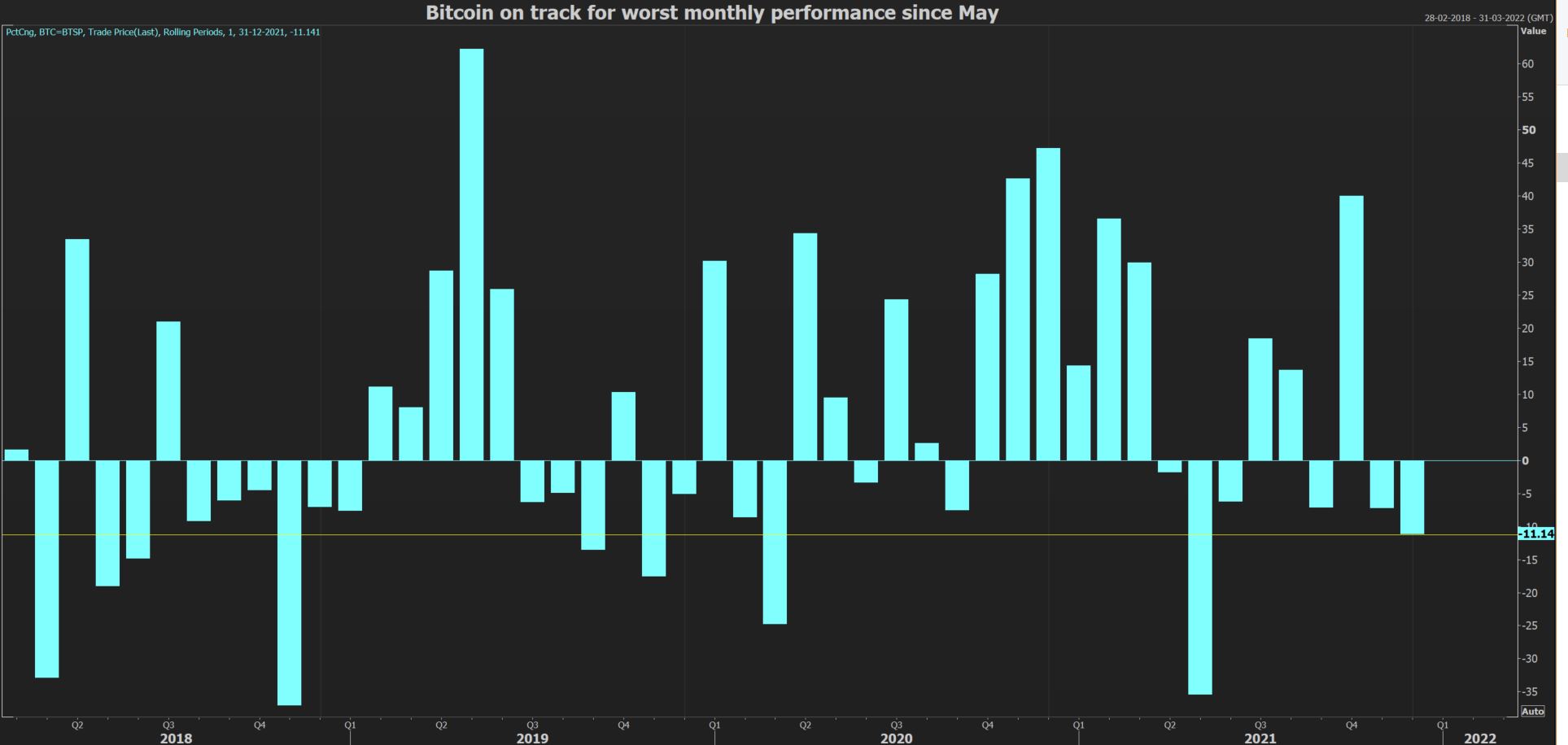

Still, it looks to be a rather blue Christmas for bitcoin, barring any major year-end moves. The cryptocurrency has slid about 11% so far this December, putting it on track for its worst month since May.

The MVIS CryptoCompare Digital Assets 100 Index (.MVDA), which tracks a basket of the 100 largest digital assets, is on track for monthly losses of 9%.

On the brighter side, CryptoCompare notes that weekly flows in December still average around $43.4 million of inflows each week. Unsurprisingly, bitcoin-based products captured the most new money, averaging $35.6 million of net inflows.

However, ethereum has posted $18.6 million of weekly net outflows on average, the only digital asset tracked to do so. Meanwhile, products tracking solana, the internal cryptocurrency of the solana blockchain that is seen as a potential ethereum competitor, saw an average of $10 million in weekly inflows in December.

Meanwhile, assets under management in Greyscale investment products dipped 17.1% to $43.9 billion, as per CryptoCompare data. Greyscale products still hold the lion’s share of the digital asset investment market, with a market share of 76.2% of total AUM, but they have lost some ground from the 86.6% they held at the start of 2021.

(Lisa Mattackal)

*****

WILL MONEY VELOCITY BE A BIGGER INFLATION FACTOR IN 2022? (1336 EST/1836 GMT)

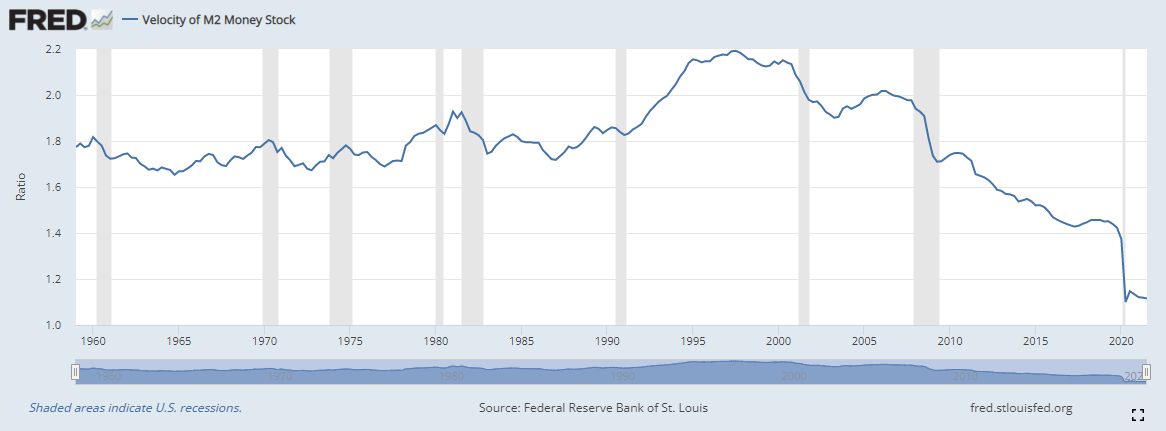

In the scary inflation days of yore, let’s call it the 1980s, runaway prices and wages were accompanied by ballooning money supply and turnover of money. But in this inflation cycle that is proving less transitory than the Federal Reserve predicted, velocity of money has scarcely budged from the lowest levels since at least the 1960s, according to the St Louis Fed.

That could change in 2022, according to Jim Caron, portfolio manager and head of global macro strategies for the global fixed income team at Morgan Stanley Investment Management. If it does, because, monetarists hold, inflation is a function of money supply times velocity, inflation could stay elevated even as some of the temporary influences now lifting prices wear off.

“We are in a position where we have very, very high money supply, so if velocity picks up even a little bit it can have an exaggerated impact on inflation,” Caron said, adding that inflation measures should come down next year, but stay relatively elevated.

The Commerce Department on Thursday said that in the 12 months through November, the so-called core PCE price index favored by the Fed accelerated 4.7%. That was the largest increase since February 1989 and followed a 4.2% year-on-year advance in October. read more

“The Fed has a goal for this time next year of core PCE at 2.6%. I’ve got the over on that,” Caron said on Monday. “Not over by a lot, but I’d say 3-3.5%.”

His reasoning is that the growth in money supply has been a product of pandemic stimulus, more than of demand for dollars to spend. Lots of the stimulus funds have gone into paying down debt and saving accounts instead of creating economic activity.

If government largess ebbs in the new year, especially if the Biden administration’s Build Back Better program fails to make it through Congress, any growth in money supply could transition to banks making loans for specific spending purposes by individuals and companies.

“You probably took out that loan for reason, to go out and do something with that, and that is where the velocity comes in. Whereas if the government just gave you a check, you got a check.”

(Alden Bentley)

*****

IMPROVING CONFIDENCE COULD SPELL BAD NEWS FOR THE GREENBACK(1223 EST/1723 GMT)

The U.S. dollar is trading at a high premium relative to its fundamentals as investors fret over the spread of the Omicron COVID-19 variant and high inflation. But that is unlikely to last, with risks to the currency rising next year, according to The Leuthold Group.

The greenback typically trades with a strong positive correlation to consumer sentiment, however this relationship reverses when confidence is replaced by fear and then panic, as is currently the case, James Paulsen, chief investment strategist said in a report.

In fact, the safe haven premium currently priced into the U.S. currency is nearly 40%, the second highest level since 1988. “This strongly suggests the U.S. dollar is poised to decline next year,” Paulsen said.

Heading into 2022 investors are concerned about COVID and high inflation but “there is a decent chance some semblance of victory will be declared over both, which would likely boost confidence and cause the safe-haven premium to evaporate.”

The Omicron variant so far appears to be far less virulent than Delta, and there are more tools and treatments now that can address the virus. The pandemic is also likely to morph into an epidemic, which should help ease supply chain problems, reduce inflation pressures and improve confidence, Paulsen said.

That may mean that the dollar will see a year of renewed weakness, which would boost commodity prices and possibly keep inflation above the Federal Reserve’s 2% target, with 10-year Treasury yields possibly rising above 2%, Leuthold said.

(Karen Brettell)

*****

ONE-MONTH HIGH FOR THE STOXX (1134 EST/1634 GMT)

Optimism about the economic recovery and a limited fallout of Omicron has brought a festive mood back to markets.

In Europe that has pushed the STOXX 600 (.STOXX) equity benchmark up by 1% to its highest in one month with banks and travel stocks leading the way in a broadly positive market.

The index is now just 1.5% far away from the record high of 490.58 hit in November before the new highly infectious COVID-19 variant spooked markets.

(Danilo Masoni)

*****

SANTA CLAUS RALLY LIKELY STILL ON THE WAY (1103 EST/1603 GMT)

Investors upset that stocks haven’t taken off enough for a Christmas rally shouldn’t fret, Santa Claus is likely still coming to town.

Stock market strength in December is typically known as a Santa Claus rally, however the term is misunderstood and strength typically comes in the last 5 trading days of the year, and first two days of the new year, according to LPL Financial.

That means it is due to start on Monday, which is also the last day a Santa Claus rally can start and the latest it has started over the last 11 years. While the rally is not a sure thing, stocks have rallied during this period 78.9% of the time, with an average return of 1.33%, which is the third best performance of the year, LPL said.

“Why are these seven days so strong? Whether optimism over a coming new year, holiday spending, traders on vacation, institutions squaring up books – or the holiday spirit – the bottom line is that bulls tend to believe in Santa,” LPL’s chief market strategist Ryan Detrick said in a note.

If Santa fails to show, however, it would likely portend a weak January. In the six instances that the Santa rally failed to materialize since the mid-1990s, five were followed by a dip in January and only one had a solid gain for the year, LPL said.

“Should this seasonally strong period miss the mark, it could be a warning sign,” Detrick said.

(Karen Brettell)

*****

S&P 500 ON TRACK FOR RECORD FINISH (1004 EST/1504 GMT)

Wall Street’s main indexes are higher Thursday morning after early data suggested the Omicron variant of the coronavirus was less severe than feared.

With this, the S&P 500 index (.SPX) is pushing over 4,720, which puts it on track for a record finish above its 4,712.02 Dec. 10 close. The SPX record intraday high was 4,743.83 on Nov. 22.

Meanwhile, the U.S. 10-Year Treasury yield is back up to challenge the 1.50% level, and value (.IVX) is slightly outperforming growth (.IGX).

All major S&P 500 sectors are rallying with more economically sensitive groups out front.

Under the surface, chips (.SOX), banks (.SPXBK) and transports (.DJT) are also among outperformers.

The NYSE FANG+TM index (.NYFANG) is slightly red.

Here is where markets stand early on Thursday:

(Terence Gabriel)

*****

VOLATILITY IN THE TIME OF OMICRON (0927 EST/1427 GMT)

As the last trading day before Christmas gets underway, the S&P 500 has posted moves of at least 1% in either direction for the four straight prior sessions — rising by at least 1% for past two days, after falling by at least that amount in the two days before.

Indeed, the benchmark index has swung by at least 1% in nine of the 16 full sessions so far in December.

As it stands, the S&P 500’s average move of 1.1% would make it the fourth-rockiest December since 1987, according to Art Hogan, chief market strategist at National Securities. Only 2018, 2008 and 2000 had bigger average December moves, per Hogan.

Hogan says in a note that the volatility stems from “three well disseminated concerns”: a more hawkish Fed, the “shelving” of President Joe Biden’s “Build Back Better” investment bill, and fears the spread of the Omicron coronavirus variant could derail the economy.

Yet even with that volatility, as of Wednesday’s close, the S&P 500 was up 2.8% in December, and 25% for 2021.

Hogan writes: “With many of the current market concerns well known, and arguably well priced in at both the index, and more prominently at the average stock level, we would suggest markets have done an overly efficient job in selling the rumor, and will likely start buying the news.”

(Lewis Krauskopf)

*****

NASDAQ 100: ON THE FLIP SIDE OF A FLOP (0900 EST/1400 GMT)

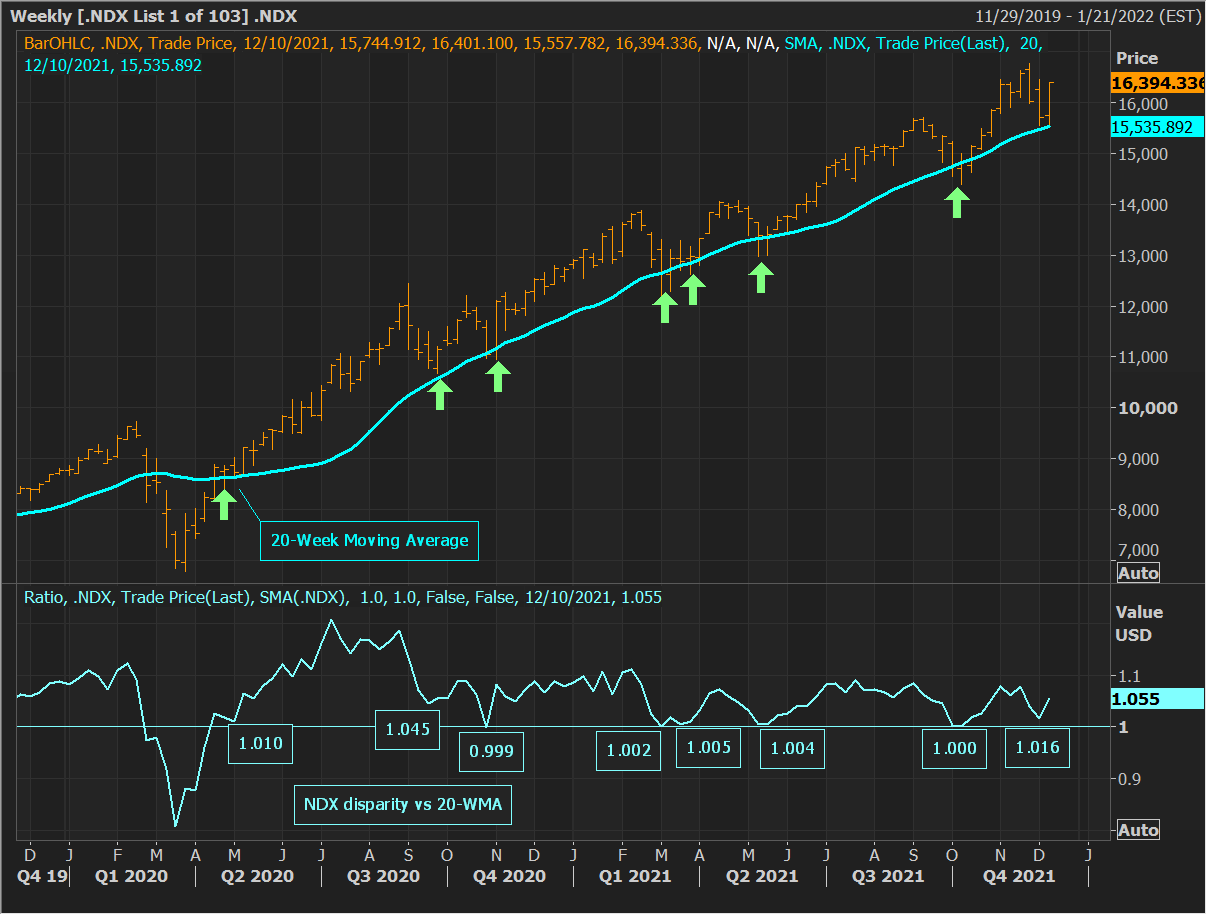

The Nasdaq 100 (.NDX) is currently up 0.27% for the month of December. That puts it on track for its smallest monthly rise since November 2016.

That said, it’s not that there hasn’t been volatility this month. In fact, there has been significant flip-flopping on a weekly basis. This week, the NDX is on track to rise 2.4%. read more Over the preceding three weeks, the index of the one hundred largest non-financial companies on the Nasdaq fell 2%, surged 4%, and then slid 3.2%.

Of note, on the downside, the rising 20-week moving average (WMA) has proven to be resilient support since it was reclaimed in April 2020 read more :

More recently, the early-December 4% surge came after an NDX slide that ended just 1.6% above the 20-WMA. This week’s rally is coming after the index declined and finished last Friday just 1.5% above the moving average.

Meanwhile, the 20-WMA, which is now around 15,625, will likely ascend to around 15,680 next week. A resistance line from the July 2020 20-WMA disparity high will then be residing around 7.1% above the moving average, which will equate to around 16,793 on the NDX.

This should add to the wall of resistance at the NDX’s Nov. 19 record close of 16,573.343 and Nov. 22 record intraday high of 16,764.855. A disparity break out above the resistance line could suggest the NDX could accelerate further into record-high territory.

Conversely, a more decisive closing break of the 20-WMA than was seen in late-October 2020 (or more than -0.1%), with the moving average then ticking down, could instead lead to a sea change in trend, to the downside. read more

(Terence Gabriel)

*****

FOR THURSDAY’S LIVE MARKETS’ POSTS PRIOR TO 0900 EST/1400 GMT – CLICK HERE: read more

Register now for FREE unlimited access to Reuters.com

Terence Gabriel is a Reuters market analyst. The views expressed are his own

Our Standards: The Thomson Reuters Trust Principles.

from WordPress https://ift.tt/3J8ygnA

via IFTTT

No comments:

Post a Comment